The accounting profession is evolving primarily because of technological advancements. Gone are the days of lonely financial experts crouched over enormous, dusty ledgers or spreadsheets, ceaselessly crunching figures. Instead, people maintain their finances using accounting software and other cutting-edge technology such as blockchain.

Almost every industry is using blockchain technology to revolutionise and innovate. Finance and accounting are two of the most prominent professions embracing this trend.

Digital technology influences accounting lik other domains, although. Blockchain, a relatively new technology, essentially eminates from accounting.

Here are some use cases on the blockchain ecosystem and how it will impact accounting in 2022 and beyond.

Table of Content

What is Blockchain?

It is an open and distributed ledger that can effectively and securely record transactions between two parties. A peer-to-peer network administers a blockchain by following a protocol for validating new blocks.

Fraudsters cannot change the data in any given block retroactively without affecting all following blocks, which necessitates collusion from the network majority. This effective regulation of how a blockchain works facilitate transaction flow, improves the double-entry accounting system and reduces cybercriminal prey.

The ease in setting up blockchains makes them appealing to businesses operating in areas lacking infrastructure for transferring large-value contracts or significant sums of money.

Check our blogpost on : Blockchain Technology and its Potential Impact on the Audit & Assurance Profession.

The adoption of blockchain technology, AI and, remarkably, machine learning is rapidly increasing. These technologies have the potential to transform the accounting sector.

Governments are increasingly enacting blockchain-related tax legislation. It indicates that they are taking blockchain more seriously and that you should as well.

Accounting and blockchain

People will not forget accounting with technological advancements. Blockchain is, in fact, the ideal technology for accounting and finance and is the only technology on the earth linked with accounting standards.

Because of the technology’s immunity, it provides to the accounting equation precisely what it requires: verification and reliability.

Regardless of the meticulous double-entries, records must still be examined and audited by third-party, independent auditors. It is a time-consuming operation that significantly raises the accounting costs of any company. And it is just here that blockchain technology’s extraordinary transparency can assist you.

When blockchain technology combines with existing accounting software, it has far-reaching implications for every sector. It helps create a more simplified, more robust accounting sector that focuses on the everyday chores of calculating numbers by redefining accounting.

With a growing demand for high-quality human added value and intellectual power, blockchain might be the catalyst that propels the accounting profession to new heights.

Use cases of blockchain technology in Accounting

The use of Blockchain technology has numerous advantages. It enables digital data to be widely circulated and accessed but not modified, making it a very dependable source of first-hand information. It also allows for the development and trading of cryptocurrencies such as Bitcoin.

But how does it assist the accountant of today? Here are some of its use cases:

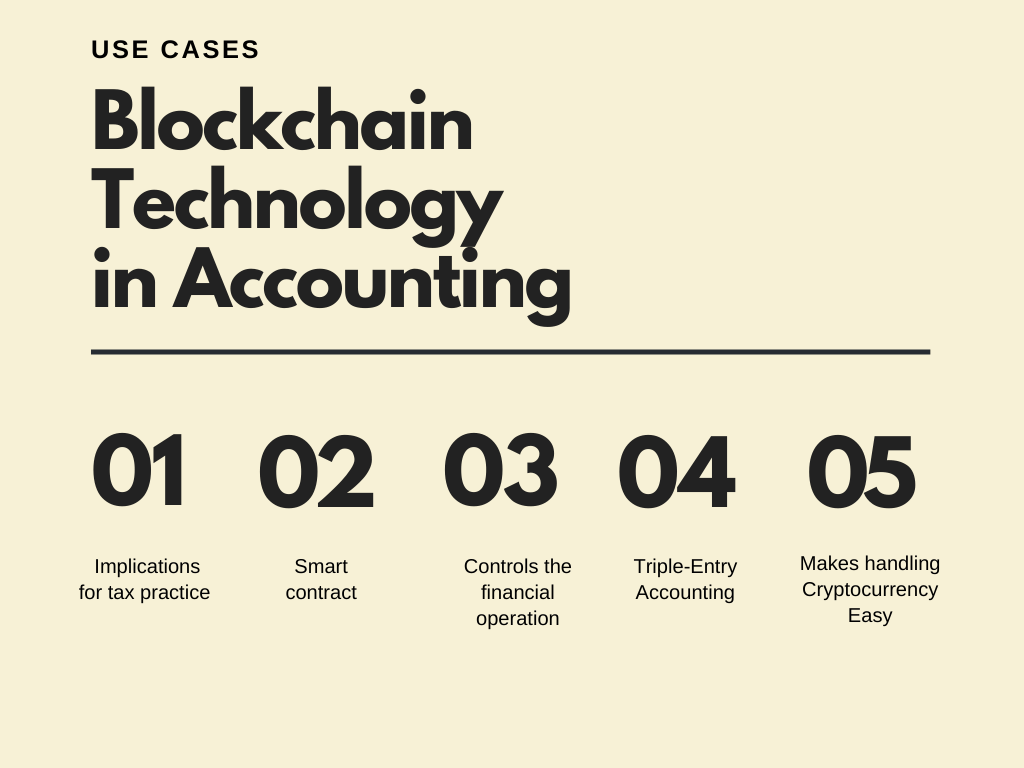

1. Understand the implications for tax practice

The decentralised structure of blockchain also aids in serving as proof that a transaction took place.

We used to rely on paper receipts to prove that a transaction took place. It will be a little more difficult to mess with Paper receipts. Digital receipts are more accessible to tamper with due to the rise of digital payments.

Blockchain technology, once again, appears to be a viable solution to this issue. The data integrity of blockchain reflects that it’s nearly impossible to change or delete a transaction once a public consensus validates it.

Blockchain’s potential tax uses are game-changing. For example, if a company uses blockchain for its balance sheets, businesses might share financial information with tax authorities.

Whether you’re working with a large MNCs or a single taxpayer, the concept stays the same: blockchain creates more detailed and accessible records than any previous technique.

Since blockchain entries cannot be tampered with, there will be a significant reduction in delays and fraud. Your efficiency will increase as your costs decrease because you won’t have to reconcile ledgers or eliminate human mistakes. You’ll have fewer administrative responsibilities to complete, allowing you to focus on more critical tasks.

2. Smart contract

A smart contract is what it sounds like: a machine-to-machine agreement with terms encoded in code. The programme takes the required action after checking all the requirements.

Smart contracts are executed and recorded using blockchain technology, which eliminates the need for any human contact. Human error or fraud is no longer a possibility.

As a finance specialist, you can ensure that a smart contract is implemented correctly. Because people rather than machines negotiate the conditions of smart contracts, you can also function as an arbitrator. If you learn how to use blockchain technology, you can open up a world of possibilities for yourself.

3. Oversee the operation

Technology can only be considered as good as the people who put it in place. You’re in a unique position to fill crucial tasks if you study blockchain and accounting.

You could, for example, become a private blockchain’s access-granting administrator. Users must have confidence in the organisation that controls the blockchain and its technology.

Some companies are working on consortium blockchains. These will be blockchains that other companies will pay to use, and service auditors will be required. You can ensure that the blockchain’s controls are functional if you understand the architecture.

4. Triple-Entry Accounting

The current accounting system is based on the double-entry system, first used in the late 1400s. In double-entry accounting, every entry to one account necessitates a corresponding and opposing input to a different account.

However, because blockchain offers triple-entry accounting, this is set to change. This approach adds a step to ensure that all transactions get recorded on a blockchain. The triple entry is designed expressly for blockchain to provide the parties involved are secure.

5. It helps in understanding cryptocurrencies

The subject of cryptocurrency is complicated, and its decentralised structure implies that accountants will eventually have to deal with many regulatory difficulties. Moreover, governments are often hesitant to fully embrace financial and monetary reforms over which they have little authority.

Accountants must be prepared to interact with customers who invest or trade cryptocurrencies. Understanding their motivations and behaviour requires some knowledge of blockchain technology.

Due to the rapidly increasing use of blockchain in financial transactions, there is a tremendous demand for tax interpretation and understanding of blockchain-related activities.

Opens Doors For New Customers

While you may have a steady stream of clients that keep your accounting firm intact, there’s no harm in diversifying your client base, and Blockchain technology can help you accomplish just that.

The Millennial generation will look to your mix of experience and skills to assist them if you demonstrate an awareness of blockchain and global trends in cryptocurrency investing. While your conventional consumers will always expect you to do things the same way you’ve always done them, the potential to diversify is a once-in-a-lifetime opportunity that you should not pass up.

How Blockchain in Accounting Can Assist Businesses

Fraudsters and scams are less likely to occur because of blockchain technology. It lowers the dangers for everyone who uses blockchain technology for accounting. It also saves companies a lot of effort by reducing their time dealing with fraud or collecting money from dishonest companies.

The immutability of blockchain technology reduces the cost of regulatory compliance and allows accounting firms or auditors to conduct more efficient audits. It means it will save you and your bookkeeper a lot of time and make auditing your financial records much more accessible.

Instead of physically validating the authenticity of every transaction, auditors may concentrate their efforts on much higher-level concerns that require human critical thinking.

It will avoid tedious tasks such as verifying transaction data and manually entering data into your ledger.

Required Skills for Future Accounting Professionals

To keep up with the changing sector, the future accountant will undoubtedly need to be technologically savvy. Accountants must become skilled in utilising the blockchain as more innovative technologies advance and more organisations shift their information to such platforms to provide clients with up-to-date financial analyses and stay competitive.

Accounting professionals who want to use blockchain will need to know how to set up information transfer for ledgers, contracts, and records and use essential software applications.

Final thoughts

The nature of accounting is changing as a result of blockchain. Universal adoption is still a few years away, which is good news for you. Massive databases and robust infrastructure are required to create taxpayer blockchains, and most governments do not yet have them.

It will increase the demand for guidance on a worldwide and national scale. Initial compliance will be challenging due to the need to make adjustments for individuals and businesses. Like every other aspect of blockchain, many finance professionals would see this as a severe challenge. If you embrace blockchain technology, you’ll have another chance to become indispensable.