While old files may add to your clutter, you cannot simply discard them. Even if you never use or refer again, the law won’t allow you to shred them.

The amount of time you should preserve tax records for small businesses depends on the activity, expense, or event it records. Businesses can react to information requests more quickly if they know how long to hold tax returns and other records. Owners can also use this data to understand their businesses better.

We’ll look at several business records, why it’s vital to retain them longer, and how long you should keep them.

Table of Content

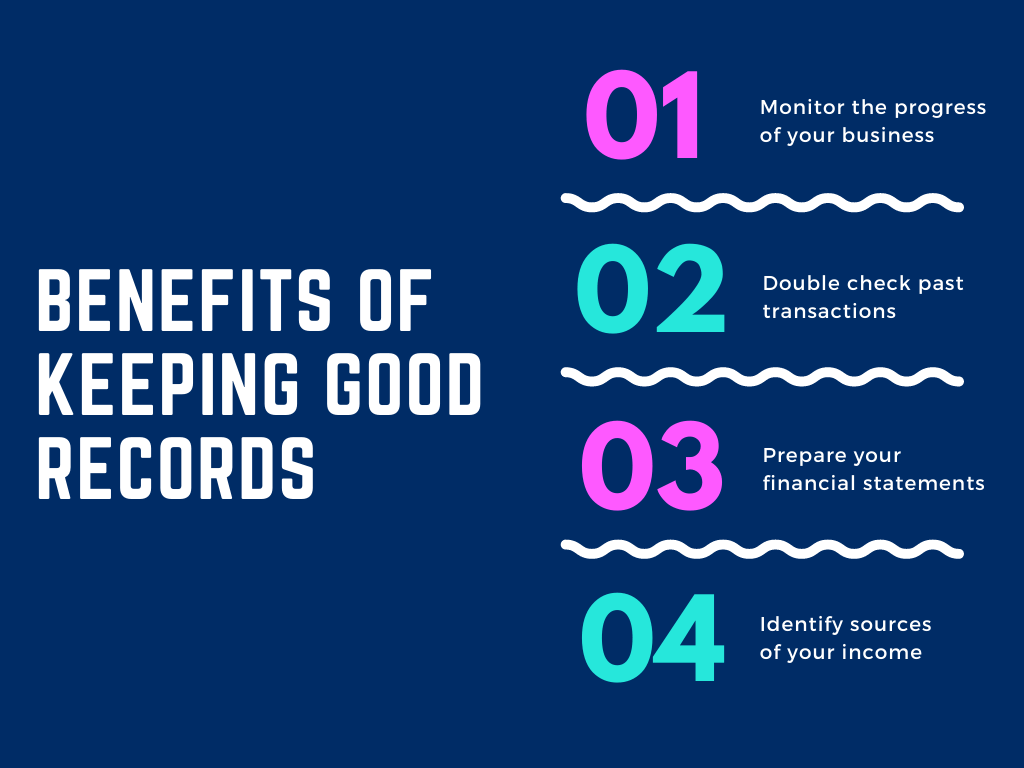

Benefits of keeping good records

Apart from your legal requirements, there are many reasons why keeping your paperwork in order is a good idea. If you need to double-check past transactions, you won’t be able to do so without good recordkeeping, especially if you don’t use online accounting software.

Even if you use online accounting software, it’s good to maintain the original records in a safe place. If HMRC decides to investigate your firm, you’ll be able to present them with a complete accounting of its finances.

A lack of physical room to retain records can affect specific organisations. The length of time you must keep your records is determined by your business structure or whether you are self-employed or manage a limited company.

Self-employed

If you’re self-employed or part of an unincorporated business partnership, you must preserve your records for at least five years after the tax year.

For example, the next 31 January will be 31 January 2022 for the 2020/21 tax return; you must preserve your records until 31 January 2027. All sales documentation, business expenses, personal income, cash put into and withdrawn from the firm, and VAT and PAYE information, if applicable, are included in these documents.

However, you may need to keep your records longer than the time limit stated above in some circumstances. For example, if HMRC is conducting an investigation, you must keep your records until it ends; similarly, if you have filed your tax returns late, you must keep your records longer.

Bank statements, sales receipts, purchase invoices, chequebook stubs, and VAT documents are commonly required. If you’ve received a government grant, you should keep the paperwork for four years from the day you received it.

Tax records

The official HMRC policy on preserving records is known as the six-year rule.’

They’ve indicated that documents about sole trader self-assessment tax, limited company accounts, VAT, or corporation tax should be accessible for six years following the tax year they relate.

It applies not just to business owners who prepare their tax returns but also to their accountants and consultants.

Limited companies

Limited firms have slightly different rules, and there is additional paperwork to consider. Limited company directors must also keep other documents, such as details of business assets, liabilities, loans secured against the company’s assets, shareholder transactions, etc.

You must keep firm records for six years after the accounting period. However, you must maintain some documents for ten years, such as:

- The statutory books of the firm

- MOSS (Mini One-Stop-Shop) records for VAT

- The minutes of board meetings and resolutions

Transaction records

HMRC has also specified that if certain records apply to specific types of transactions, you must maintain them for six years or longer. These records include:

- For a corporation, a transaction occurs over several accounting periods (for example, if a bank statement covers six months which applies to two separate tax years).

- It also includes a purchase made by a firm that can last longer than six years, such as equipment, a car, or machinery.

If the company tax return was late, it is under tax audit, or HMRC has launched a compliance inspection on a tax return for your customer, you should maintain client documents for longer than six years.

Employers

Employers are required to preserve all PAYE records for three years (in addition to the current year).

You should keep the following documents:

- Payments made to employees.

- It also includes any deductions from your employee wages of Income Tax, National Insurance contributions (NICs) and Student Loan payments.

- Details of employee benefits and expenses.

- Tax code notices.

Partnerships & Sole traders

You must keep the following records if you are self-employed and do not operate through a limited company:

- A sales records and takings, including cash collections.

- All purchases and expenses.

- VAT records, such as VAT sales and purchase invoices, import and export papers, and other information about your VAT account.

- If you employ someone, keep PAYE records.

After the 31st January submission deadline of the applicable tax year, you must maintain these records for at least five years.

Client management

You may want to keep the records that apply to specific clients as long as they employ your practice for good client management.

When your professional connection ends, it’s a good idea to hand over the documents to the customer to continue to have access to them if they need them. You could hand them over and explain that any residual records leftover will be destroyed after six years, just in case.

You might decide to maintain all of your clients’ records, even after leaving. With more forms becoming digital, it could be a useful security measure, as there are a few situations where documents are required:

- HMRC can pursue a client for tax, interest, or penalties owed over the previous twenty years.

- Evidence needed for criminal offences committed by your practice or a client has no expiration date.

- You should keep any files relevant to criminal proceedings.

Construction Industry Scheme (CIS)

According to the law, you must keep the following information:

Contractors – Payments made to all subcontractors for work completed and items acquired by subcontractors.

Sub-Contractors – Details of all payments and deduction statements for subcontractors. For example, Copies of invoices sent out and payment statements received.

You should keep these records for at least three years after the tax year they apply.

What’s the best way to store records?

Anyone who has ever had a rail season ticket knows how delicately printed receipts are. A few weeks at the bottom of a wallet can render most documents illegible.

Six years of records is a significant quantity of paperwork for a company that generates a lot of expenses.

HMRC advises that you save all original documents that you receive. It does not imply that they must be in paper form. Most records can be scanned and stored electronically on a computer or a storage device like a CD, memory stick, or cloud.

It’s also essential to scan the opposite side of any receipt with information on it, as many stores produce double-sided tokens. Ensure to have easy access to the digital copies if HMRC makes a request.

HMRC requests that you maintain the original documentation proving your tax deduction if you’re an employee, such as your P60 form from your employer (which shows your pay and tax information for the tax year).

It’s also worth noting that “scanned” does not necessitate the purchase of a scanner; as long as all of the information is legible, a photo taken with your smartphone will suffice.

What about paperless offices?

The Civil Evidence Act of 1995 also specifies that electronic documentation has the same weight as a physically signed document. Thus, all digital documents shall be stored securely for six years, like paper records. Once this period has gone, the digital recordings can be destroyed/deleted at the appropriate time or maintained for security or legal reasons if HMRC or the courts require documents as evidence.

Scanning your receipts and backing them up online is a far better option for these and other reasons. These days, HMRC even encourages firms to preserve their records digitally.

Who should keep track of the invoices?

The business owner’s responsibility is to guarantee that the records are kept accurately. HMRC will not accept any explanations for missing paperwork.

Finding a simple solution for organising invoices and receipts that is both time-saving and practical for business owners and startups can be complex.

Finding a simple solution for organising invoices and receipts that is both time-saving and practical for business owners and startups can be complex. The digital transformation of enterprises, on the other hand, has transformed productivity and convenience. There are many tax record bookkeeping software available on the internet; select one according to your requirement.

Make a backup of your invoices if you aren’t utilising invoicing software to preserve them.

Final thoughts

In conclusion, unless you have a burning urge to destroy your tax documents as soon as legally permitted, we recommend keeping your records safe for at least 6+ years.

If any business records are lost or stolen, you must immediately notify HMRC. They may request that you attempt to replicate the documents, but you might face financial penalties if you fail to present the relevant records when requested.