The triple-lock pension scheme is the government’s commitment towards retirees to safeguard their pensions during inflation. Many of the retired community suffer from poverty and have a poor lifestyle. The UK government implemented this state pension policy to upgrade their living standards in 2010.

However, the triple-lock pension scheme is about to be modified after the Coronavirus outbreak in the country. It is estimated to become too expensive to maintain by the government.

Table of Content

What is a triple lock pension?

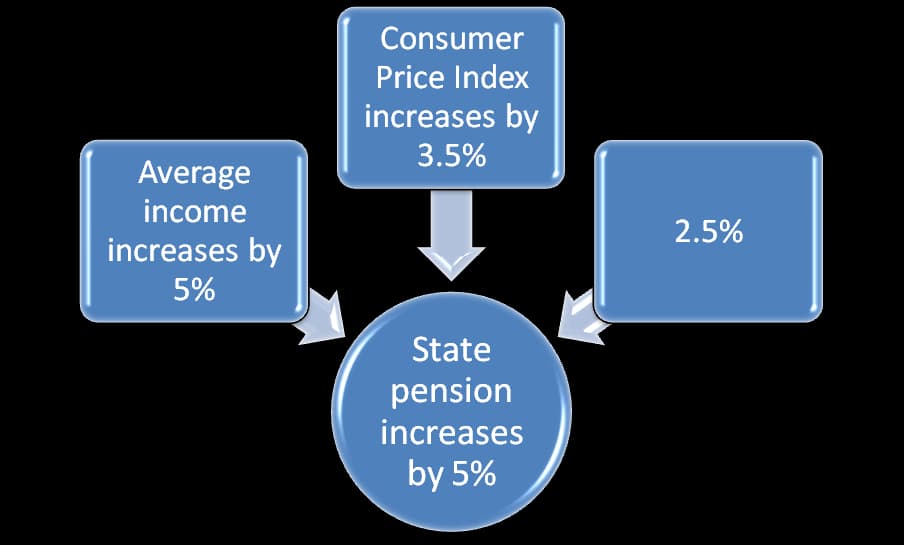

A triple lock pension is a government’s commitment towards retirees to raise their pension level annually. Three measures decide the increase in the state pension of a retiree, hence triple lock.

The highest of the three different criteria given below adds to the current pension amount:

● Average growth of wages every year,

● A minimum of 2.5%, or

● Inflation measured by the Consumer Prices Index

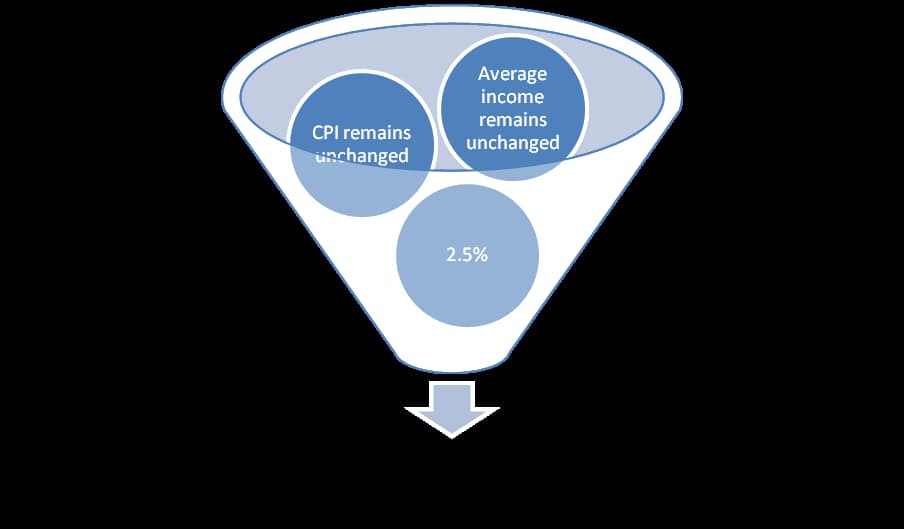

That means if your average income increases by 5%, your state pension will be 5% as well. When average income and CPI remain unchanged, state pensions increase by 2.5%.

Let us understand triple-lock pensions with the following diagrams:

How does triple lock affect you?

As a young employee, you may wonder what is state pension triple lock? But, If you are receiving a state pension, you know how vital a triple lock is for your livelihood.

The Conservative-Liberal Democrat coalition in 2010 proposed the state triple lock pension to keep the retirees above the poverty line. However, it became a burden for the government in later years.

The government suspended the triple lock for the 22 tax year and became a double lock instead. The pension increased by 3.1%, higher of a minimum of 2.5% and CPI. The government argued that many people were coming out of furlough after the pandemic, and it distorted wage growth %.

The Chancellor in 2022 autumn statement has confirmed that triple lock is coming back in 2023.

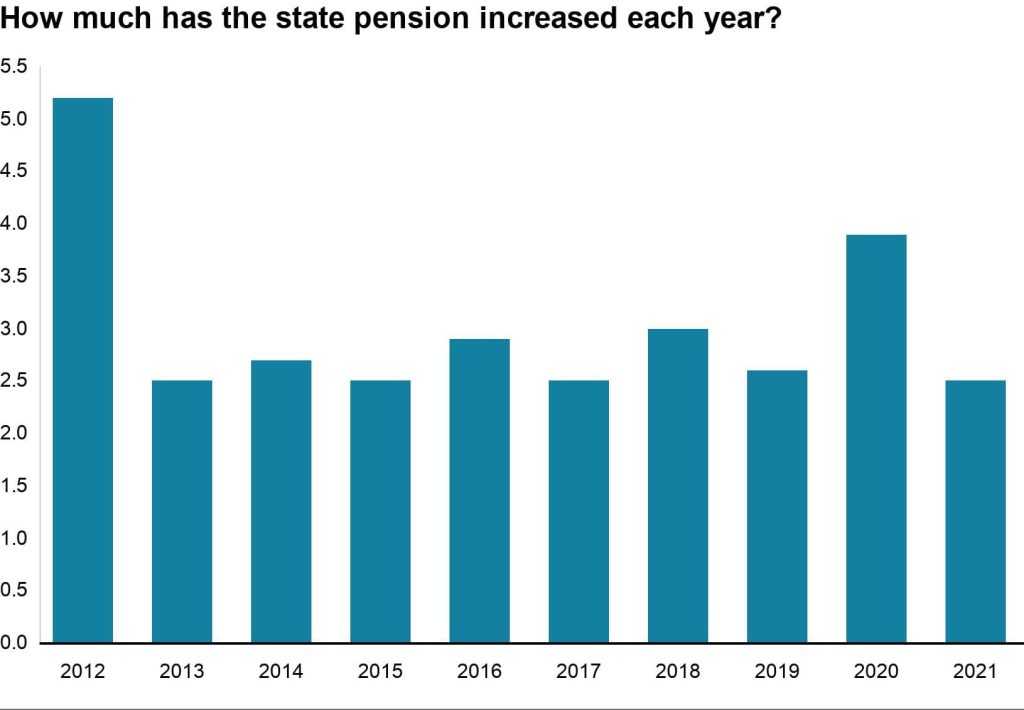

In the below table, we can see which of the factors in the triple lock is affecting the pension:

| Years | CPI | Average Income | Guaranteed minimum | Which part of the triple lock triggered the state pension |

| April 2012 | 5.2% | – | – | CPI |

| April 2013 | – | – | 2.5% | Guaranteed minimum |

| April 2014 | 2.7% | – | – | CPI |

| April 2015 | – | – | 2.5% | Guaranteed minimum |

| April 2016 | – | 2.9% | – | Average income raise |

| April 2017 | – | – | 2.5% | Guaranteed minimum |

| April 2018 | 3% | – | – | CPI |

| April 2019 | – | 2.4% | – | Average income raise |

| April 2020 | – | 3.9% | – | Average income raise |

| April 2021 | – | – | 2.5% | Guaranteed minimum |

To understand the above table, we have taken a graph to see the rise and fall pattern in the state pension.

In 2013, 2015 and 2015, the state pension increased by 2.5% when the prices and income were not changing. That means the pensioners were earning more than the working group.

From April 2010 to April 2016, there was an approximately 22.2% rise in the state pension compared to growth in earnings and CPI or consumer price index.

Hence, the triple lock pension has an impact on your life. Additionally, you can beat inflation when the government promises to pay a guaranteed minimum of 2.5% on a pension. So, your retirement fund increases over time.

What else?

A triple-lock pension changes your spending structure.

Inflation directly impacts the cost of living of an individual in the UK. The CPI keeps track of the rise and fall of every household’s essential goods and services.

Suppose the CPI is 5%, and your state pension fails to cope with the inflation, your money drains and empties your pocket. Also, to save money during inflation, you need to reduce purchasing some essential items.

The life expectancy of an individual varies. The state pension you receive may not fulfil all your needs from retirement to death. However, a triple lock pension can meet the increasing cost of goods and services.

How to protect yourself from such suspensions?

It would be best not to depend only on government allowances, as they can change over time. Therefore, you must have a separate retirement fund or make investments in the initial years.

Investment in the early days is a great choice. You can earn more, and instead of increasing the spending, purchase stocks in the market and sell them at higher prices later. Then, pool the money in a separate pension account to avoid personal expenses.

You can ask a professional to settle your accounts and help make a separate retirement fund.

Conclusion

A triple lock pension is an advantage for retirees to spend their life without compromising their needs.

Individuals must start saving money from the early stages of employment. That savings will be of great use after retirement. In addition to that money, the government pension will act as an add-on.

However, before you decide, you must speak to a professional. Experts know the government’s latest rules and regulations and guide you to a better retirement planning program.