Accurate bookkeeping is essential in determining your company’s internal and external health. The financial statements generated at the end of the accounting cycle can assess your company’s viability and long-term financial health in all areas.

This cycle can benefit businesses in various ways, regardless of whether it’s a tiny business or a cash accounting system. It ensures that the balances are accurate by providing that you haven’t skipped anything during the procedure.

When you’ve completed all of the processes, you’ll be able to start fresh with the next accounting period. Here’s an overview of the accounting cycle for small businesses, covering the eight main methods.

Table of Content

What is the Accounting Cycle?

The accounting cycle is an eight-step method for performing bookkeeping activities in a business. It gives a step-by-step process for documenting, analysing, and reporting a company’s financial activity.

The reporting requirements will determine the length of the accounting cycle. The majority of businesses strive to evaluate their performance every month; however, some may place a greater emphasis on quarterly or annual outcomes.

Regardless, most bookkeepers are aware of the company’s financial situation daily. Overall, setting the length of each accounting cycle is critical since it establishes particular opening and closing dates. When an accounting cycle ends, a new one begins, resuming the eight-step accounting procedure from the beginning.

What is the importance of the Accounting Cycle?

As we’ve seen, the accounting cycle maintains your paperwork neat and orderly. It enables you to keep precise and professional financial records.

But why do they need to be so well-organised in the first place? Because of three significant factors:

- To assist you in analysing the performance of your company. Financial statements provide you with an eagle-eye view of your company’s finances. They help you determine the effectiveness of a previous financial strategy or how much money to set aside for future purchases.

- To assist you in raising additional funds for your company. If your company intends to raise funds in the future, you’ll need to show reliable financial accounts to potential investors. And the best way to have accurate financial records is by following the accounting cycle.

- It ensures that your company complies with government legislation and accounting requirements. These are a collection of rules that you must follow as a business owner.

The government, for example, expects you to prepare your financial records and pay taxes based on your earnings. That is what you can accomplish with the accounting cycle.

Understanding the 8-step Accounting Cycle

The eight-step accounting cycle begins with the individual recording of each transaction and concludes with a complete report of the businesses’ actions throughout the cycle period.

Depending on the system at each organisation, you may use more or less technical automation. Although bookkeeping typically requires some technical assistance, a bookkeeper may be necessary to intervene in the accounting cycle at various times.

The eight-step accounting cycle will almost always need to be modified to meet any specific company’s business model and accounting procedures.

Businesses can also select whether to use single-entry or double-entry accounting. They must use double-entry accounting to create all three primary financial statements: the income statement, the balance sheet, and the cash flow statement.

Accounting Cycle steps

The accounting cycle has several variances, particularly between cash and accrual accounting. There are several that have eight, nine, or even ten steps. We’ll break it down into eight steps for simplicity’s sake.

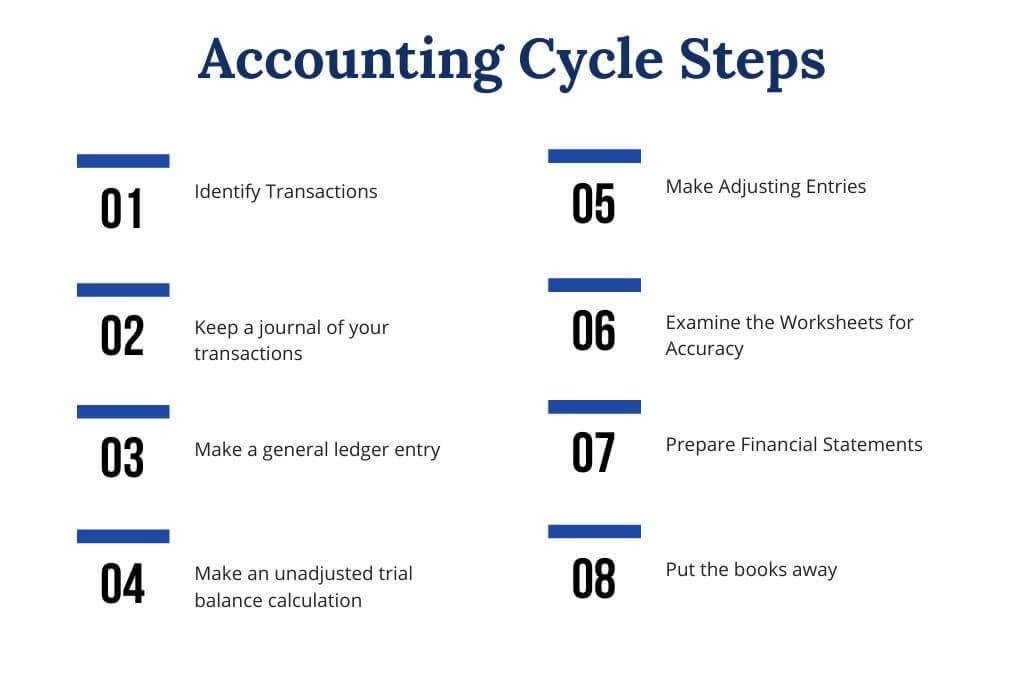

1. Identify transactions

Reducing all of the information you have on each transaction within a specific time is the first stage in the accounting cycle.

Consider your company’s accounting methods; if you employ the accrual approach, you’ll record transactions as soon as they happen, regardless of whether or not you have cash on hand. If you use the cash method of accounting, you’ll keep track of transactions as soon as cash changes hands.

You can scramble to gather receipts hours before the deadline if you don’t have a professional bookkeeper on hand throughout the reporting period. During an accounting period, a company will have a lot of transactions. These transactions would trigger the start of the cycle.

2. Keep a journal of your transactions

The next step is to enter your financial transactions into your accounting software or ledger as journal entries. Some businesses combine steps one and two by using point-of-sale technology linked to their books.

Regardless, keeping track of spending is critical for organisations. When you identify expenses and income, it depends on the form of accounting you use and how you do it.

Double-entry accounting recommends documenting every transaction as a credit or debit in separate journals to keep an accurate balance sheet, cash flow statement, and income statement.

On the other hand, single-entry accounting is more akin to keeping track of a cheque book. It provides a balance report rather than requiring repeated submissions.

3. Make a general ledger entry

Post all your financial data, including your company’s total debt and credit balances, to an all-encompassing ledger account. This ledger compiles all of your financial details into one convenient location. Most accounting software will take care of this for you automatically.

However, if business owners and their accountants and bookkeepers want, they can still use pen and paper to complete an accounting spreadsheet.

4. Make an unadjusted trial balance calculation.

While you’ll calculate the unadjusted trial balance once you’ve identified, recorded, and posted all transactions within the accounting period, you’ll figure it out after the period finishes.

The trial balance determines the unadjusted balance of each account. After then, the balances are tested and analysed in the next stage.

An unadjusted trial balance is essential for a firm because it ensures that your financial records, total debits, and credits are equal. If they don’t, it’s because something is missing or misaligned.

This stage identifies irregularities, such as payments that were supposed to be collected and cleared but weren’t.

Regardless of the situation, an unadjusted trial balance shows all your credits and debits in a table.

5. Make adjusting entries

Adjusting entries can help to change already recorded journal entries. Their goal is to ensure that the financial statements contain only current and relevant data. Deferrals, accruals, and estimates are the three primary forms of modifying entries.

Deferrals are funds spent before receiving actual revenue or service. Prepaid expenses and unearned revenues are examples. When you pay for a future asset, such as insurance, this is known as a prepaid expense.

On the other hand, accruals are money received before the work is completed and declared a liability. A good example is your yearly newspaper subscription.

Cash earned but not yet received is referred to as accrued revenue. A transaction is recorded as accumulated revenue if a customer delays payment for a month. On the other hand, Accrued expenses have been incurred but not yet paid. Paying your employees’ salaries at the end of the month is common.

Finally, there are estimations. When you can’t determine the exact value of non-cash objects, you have to make an estimate.

The depreciation expense is a standard business estimate. Long-term assets, such as buildings or equipment, are depreciated over their estimated useful lives.

We use a formula to estimate it because the exact depreciation cost is impossible to calculate in cash. The money spent is divided over several accounting periods depending on how long the asset’s useful life is.

6. Examine the worksheets for accuracy

This step is only required if the final balance do not match. Mathematical errors, wrong posting, and inaccurate transcriptions are the most common causes of accounting errors. Whatever the situation, a bookkeeper must determine the source of the error.

For example, if the debt is £200 and the credit is £1,000, the bookkeeper should fix £800.

On the other hand, accounting software makes it far more difficult to make mistakes. The software will detect it and notify you of the discrepancy even if you do.

7. Prepare financial statements

The direct and formal yearly reports are financial statements. Corporate management communicates financial information to all stakeholders through these basic accounting statements.

Owners, managers, and employees are among these stakeholders, as are other external parties such as investors, creditors, tax agencies, and the government.

Such consumers make financial decisions on principal accounting statements based on the entity’s financial situation, operating performance, and financial health.

8. Put the books away

Now that you’ve arrived at your post-closing trial balance, it’s time to move all of the information from your temporary accounts—the ones that only affect this accounting period—to your permanent records, which reflect your company’s overall condition.

The accounting cycle ends now, only to begin again with the next accounting period.

Final thoughts

The accounting cycle is a series of steps that result in a detailed report on a company’s financial performance. Businesses must complete the accounting cycle once every accounting period, quarterly, yearly, or other periods depending on legal requirements.

The accounting cycle can be challenging for business owners who do not have an accounting or bookkeeping background. As a result, we propose hiring a professional accountant to handle everything for you. You can better use your time, energy, and resources on other aspects of your business if you hire a professional.