Bookkeeping is a topic that many new business owners leave till the accounts and tax return submission deadlines. Though the issue is highly complex for the new and small business owners, avoiding it invites more trouble.

This article will cover the basics of bookkeeping, tips for better small business bookkeeping and beyond while keeping it simple and easy to understand.

Table of Content

- What is Bookkeeping?

- Hiring a small business bookkeeper or doing it on your own?

- Know about the bookkeeping systems

- Getting started with bookkeeping for small business

- Tips for doing the bookkeeping

- Get in touch with Experlu experts

- Are you looking for a reliable and professional Bookkeeper near me?

- Final thoughts

What is Bookkeeping?

Bookkeeping is the process of organising and recording financial transactions in a ledger. It provides accurate and timely information about the financial activity of a business.

It plays a significant role in the long-term success of any business and gives you a clear picture of your business’s cash flow.

To know more about bookkeeping and its importance, check out our blog on what is bookkeeping

Hiring a small business bookkeeper or doing it on your own?

Understanding your financial transactions and keeping track of it is the key to managing a prospering business as a new business owner.

There is no legal requirement to hire a professional bookkeeper under the Companies Act, and the decision is entirely your call.

However, you can always weigh the pros and cons of hiring a small business bookkeeper and doing it yourself.

If you have decided to do your bookkeeping, you will learn more about your business, saving money invested in developing your business. However, hiring a professional bookkeeper can save time and reduces chances of error.

Time is a finite resource and is the most critical asset of high value to all, including new business owners. It would be best if you used it to focus on business growth and strategic activities.

Furthermore, you are likely to make mistakes in bookkeeping and spend money on covering penalty fines from HMRC. Hiring an expert in bookkeeping for small business will save you money.

Know about the bookkeeping systems

New and small businesses can have a large number of transactions, and if you’re not keeping your books properly, there are chances you lose an overview.

Choosing the right bookkeeping system is very important, and knowing the types, how they work, and determining which method can fit in your business.

There are two most common types of bookkeeping systems.

1. Single entry bookkeeping system

Sole traders prefer single entry systems to record and maintain the ‘bare essentials’ like cash records, accounts payable, accounts receivable and tax paid.

2. Double-entry bookkeeping system

Small and large businesses use a double-entry bookkeeping method where every transaction requires an equal and opposite entry.

For instance, recording cash sales of £200 would require making two corresponding and opposite entries: a debit entry of £200 to the ‘Cash’ account and a credit entry of £200 to the ‘Sales’ account.

| Date | Particulars | Dr/Cr | Amount in GBP |

| 05 Aug 21 | Cash | Dr | 200 |

| Sales | Cr | 200 | |

| Recording of cash sales |

Debits and credits must always be equal. Almost all major accounting software follow a double-entry system of bookkeeping.

Getting started with bookkeeping for small business

Now that you know about it and its importance, let’s focus on bookkeeping for your small business.

Bookkeeping for small businesses is easier when compared with enterprise businesses. This is because there are fewer transactions, simple nature of workflows and systems involved.

Tips for doing the bookkeeping

Below are a few tips you can follow to start bookkeeping for small businesses.

1. Maintain a separate record of your business & personal transactions

The first step in bookkeeping is to have separate records of your personal and business transactions.

As you know, bookkeeping is all about having an overview of the movement of financial transactions within a business. Mixing up personal transactions with your business transactions will make it challenging to identify which ones belong to your business for future references.

2. Use an online cloud-based bookkeeping software

In this fast-moving world of digitisation, you want to utilise the tools out there to make your life easy.

Cloud-based software versions are preferred over Desktop ones, as you do not spend time on upgraded versions of online accounting software.

In addition, the introduction of Making Tax Digital (MTD) by HMRC in April 2019 makes it essential than ever for businesses to consider using accounting software.

A simple search on google will list hundreds of online accounting software available for all types and sizes of businesses, making it hard for you to choose one.

There is no right and wrong answer here; it all depends upon what you need from an accounting software- multi-currency, stock, invoicing, direct bank feed and so on.

3. Send invoices to customers

Filing and invoicing must be done frequently. Sale invoices and purchase bills are recorded separately.

You can sequentially file the sales invoices, and there are numerous ways to file the purchase bills.

However, ensure that your system is logical to access any document when you need to quickly.

You can send invoices to your new customers and record bills on the go with the help of cloud-based software, like Xero, Quickbooks, Sage.

4. Record bills

Record all bills in the ledger.

You can use tools like Hubdoc or Dext (formerly ReceiptBank) for data capture.

These tools use OCR or the Optical Character Recognition technology to capture all data from bills- like supplier name, invoice number, due date, amount, VAT rate and description etc.

It will save time and reduce human error. It is widely used and is a part of the daily routines of professionals dealing with a more volume of documents.

5. Perform bank reconciliation

Bank reconciliation lets you compare your internal financial records against the records provided to you by the bank.

Doing this can easily spot fraud and common accounting errors and reduce the risk of transactions leading to penalties and late fees.

6. Integrate payroll software

Payroll is one of the essential components of your company’s management.

Though many business owners opt to outsource their payroll requirements, a few owners prefer to keep it in-house. This is when payroll software comes in handy.

Payroll software is a platform that simplifies calculating the employee’s pay, filing RTI and pension and paying employees of the company.

By integrating the software, you will only need to provide the data input once, and the software will exchange it, thus reducing the manual efforts.

7. Keep records of cash transactions

Banking your cash payments daily or on a fixed frequency reduces the risk of theft. Using petty cash to pay business expenses can create problems in revenue and expenses reconciliation.

The best approach is to deposit cash in the bank and withdraw for petty cash expenses. It will leave a clear audit trail of cash movement in and out of businesses.

Every time you draw money from your petty cash, record it. Many business owners miss out on reconciling the petty cash regularly, thereby increasing the risk of misappropriation of assets.

The sooner you deposit your money in the bank, the more beneficial it is for your cash flow and business.

8. Collect cash from your customers on time

Credit control is one of the essential functions of running a successful business.

Delayed payments can harm your business and create avoidable cash flow problems. Don’t let your clients owe you money for an extended period.

Wherever possible, use direct debit and online payments to improve your cashflows.

If you offer generous credit terms to your customers, consider using invoice factoring.

Credit control ensures the timely collection of outstanding invoices.

9. Understand primary Financial reports

Understanding the primary financial reports is the next step you should take.

Find documents and bank statements related to your business transactions that can include bank statements, marketplace statements, tax reports, and other payment processor statements.

You can ease the process by using accounting software or excel templates.

The most common financial reports are:

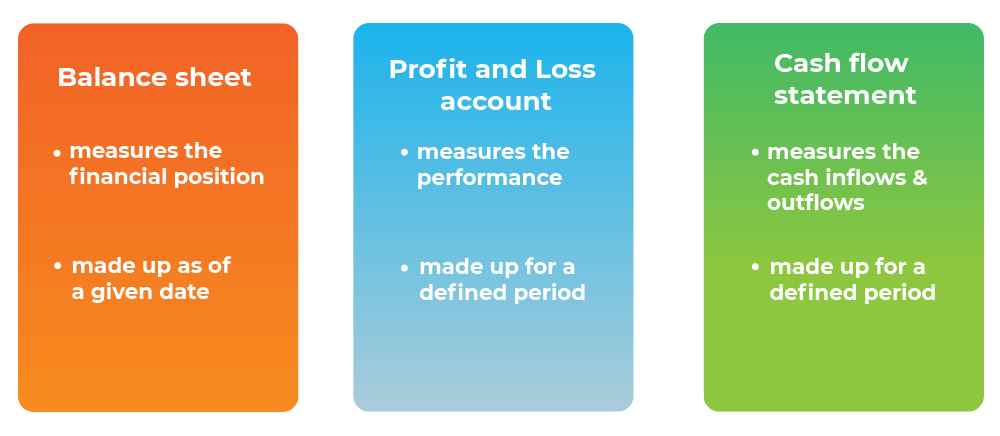

i. Balance sheet

A balance sheet is a financial statement that compiles a company’s assets, liabilities and equity at a specified period.

Assets – Liabilities = Owner’s equity.

ii. Profit and loss (P&L) account

P&L account is a financial report, also known as an income statement or income of comprehensive income.

As the name suggests, it shows net profit and loss for a given period. Businesses usually prepare profit and loss account on a monthly, quarterly, half-yearly and yearly basis.

The report is usually divided into revenue, cost of sales, gross profit, administrative expenses, operating profit, financial charges, profit before tax, taxes and profit after tax.

You calculate taxes on the profits as per this report with adjustments for specific items like depreciation, entertainment expenses and tax-deductible allowances.

iii. Cash flow statement

The cash flow statement is similar to the P&L statement. However, it doesn’t involve non-cash items.

It simply states the cash flows in and out of your business.

10. Stay updated with your bookkeeping duties

Bookkeeping is the soul of your business, however small or big it is.

Companies that practise good bookkeeping are well-administered, and any financial information needed is readily available for decision making.

The best way to remain in control of your business finances and anticipate any potential threats is to update your bookkeeping on a daily or weekly basis.

11. Stay on top of tax deadlines

Keeping up with tax deadlines can be a juggling act when you have numerous work commitments and other things to take care of.

Make sure you review your bookkeeping before the VAT filing deadline.

So, plan and set aside money for anticipated VAT and business tax bills. Avoid facing fines and pay your tax on time.

Get in touch with Experlu experts

Experts at Experlu can assist you with all aspects of small and new business bookkeeping and accounting.

We have a wide range of professional accountants and bookkeepers. Depending upon your requirement, we will begin our extensive search to match the Bookkeeper for you.

Are you looking for a reliable and professional Bookkeeper near me?

If you are looking for a bookkeeper for the first time and don’t know where to begin, you are in the right place.

Tell us about your business, and we will find you a handful of bookkeepers to choose from.

We have registered bookkeepers all over the United Kingdom who have years of expertise in bookkeeping, VAT returns, management accounting and year-end compliance work.

Our team at Experlu has set an aim to make the process of accounting and bookkeeping services as simple as possible.

We ensure that our clients stay stress-free about keeping track of their accounts and keep their key focus on growing their business.

Bookkeepers at Experlu have extensive experience and can render solid financial advice, industry-specific guidance and company planning to assist you to overcome your Bookkeeping issues.

Final thoughts

Bookkeeping is significant in any business, irrespective of whether you choose to work yourself or hire a professional to do it for you.

Bookkeepers make or fail businesses.

You can’t make strategic business decisions with inaccurate financial statements.

You can always find a reliable bookkeeper by asking other business owners for a suggestion.

Alternatively, Experlu has many qualified professionals on our directory and can put you in touch with one of the best Bookkeepers for you.